It means focusing on the value, meaning, and engagement you create for the people you serve. When utilising people’s data to create value for them, it means making sure they understand how their data is being used to create that value - and that goes beyond consent-based data sharing.

The role of financial services in building trust

But an industry obsessed with pushing products still has lessons to learn when it comes to the difference between leveraging insight and selling it.

We need to accept that people should control who accesses their data and for what purpose. We need to think of organisations as data custodians or information fiduciaries. That means that providers need to be relevant and useful and Moneyhub provides that missing link.

It aggregates, organises, and enriches data and then monitors it on behalf of the customer. Then, with an understanding of the customer context, actionable insights (or ‘nudges’) can be introduced to coach the user towards better outcomes. This might be through prompts, alerts, or new options being surfaced - it’s about helping people and for what exchange of value.

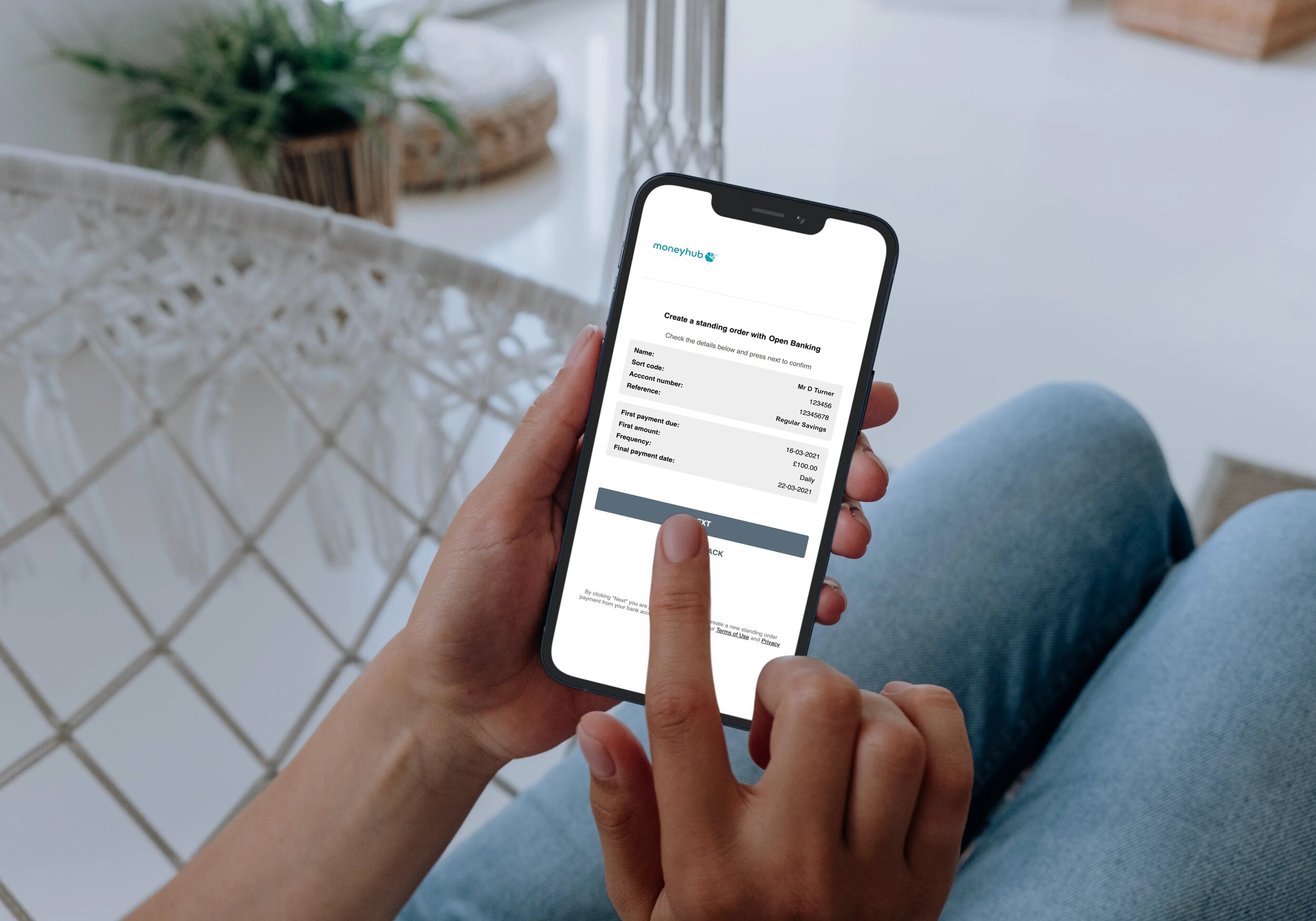

Harnessing insights to enable Open Banking payments

Insight is not an end in itself and the consumer needs the means to put in action decisions, simply and cheaply. Moneyhub uses money to savings, investments, and pensions, or to pay bills and reduce debts.

By being a trusted partner of the customer, the insight from income and expenditure analysis combines with navigation towards improved financial wellbeing. Helping customers by being the everyday financial coach, means that wellbeing is not a goal but a by-product of improved customer outcomes. Here are some of our practical examples of that in practice:

Expenditure analysis shows that the customer is paying rent. There is no sign of contents insurance - so is there an awareness of the risk associated with that? Or could that rental payment history be used to support a mortgage application?

An employer provides a range of employee discounts from retailers – as one of our clients has shown, by personalising offers based on past expenditure, the average Moneyhub user can save over GBP 70 per month, with no change in spending habits.

Consumers are keen to invest ethically and sustainably but, in addition to aggregating and scoring their investment portfolio, expenditure analysis could be used to create nudges towards greener lifestyle options or a carbon footprint offset savings plan or donation.

Impulse spending can be converted to impulse saving with an unplanned treat being accompanied by a self-imposed rule to sweep the same amount into an ISA or a pension.

Variable recurring payments can be set up when goals are met or a budget is tracked.

By adding a house price feed combined with mortgage repayments, customers can be alerted to new financing deals becoming available as the loan-to-value ratio comes down.

With 80% of employees not sure if they are saving enough and the self-employed still outside of auto-enrolment, the adequacy of pension saving can be forecasted and nudges made to help towards a better outcome, referencing current expenditure and in-retirement lifestyle.

Despite companies often having substantial customer data available, they continue to require customers to go through time-consuming and inaccurate fact-finding processes. With consent, the consumer can share their data, containing verified assets, income, and expenditure information.

Consumers can self-police by using ‘appropriate friction’ such as alerts around budget overshoots or comparing the effect of saving an amount rather than spending it.

Privacy & personalisation: a mutually inclusive relationship

By never selling customer data or taking a third-party commission on product sales, Moneyhub and its enterprise clients have always respected customer interests and balanced privacy against personalisation. The value exchange is always fair and controlled by the consumer.

Open Banking is useful but ancillary to the benefits derived from holistic Open Finance.

Critically, value creation from insight is organic and relationship- based, a far cry from crass product pushing. If a product solution is involved, it is more likely to be bought than sold and more likely to be retained as it is suitable and affordable. From here, customer centricity becomes a reality rather than a slogan - and the path from insight to value is lit by Open Finance adoption.