If you’re responsible for fraud or compliance, you’ve probably seen it first-hand; a spike in alerts, a stretched team, and too many cases that turn out to be nothing.

False positives in transaction monitoring aren’t just operational noise pollution; they directly affect costs, customer experience, and your team’s ability to focus on real threats. Expectations are only increasing in the eyes of regulators like the Financial Conduct Authority.

The FCA notes that “financial crime controls are most effective if they are calibrated to the current threats and risk”, which raises an important question. If your institution is generating an excessive number of low-risk alerts, are its controls calibrated correctly?

Each unnecessary alert diverts time from genuine risks, slows investigations, and creates friction for customers who have done nothing wrong.

In some cases, this causes blocked payments, restricted accounts, and avoidable churn; something widely linked to financial anxiety, and declining trust in user experience and financial services.

Internally, the impact builds quickly. Our own client conversations reveal that approximately 20% of call centre volume comes from transaction disputes caused by confusion, often tied to alerts that should never have been raised.

There are two ways to look at this. Some teams accept false positives as part of automated fraud detection. Others see them as a problem worth solving.

Read more: are false positives really that bad for banks?

Matt Barr, Product Director of Categorisation and Enrichment at Moneyhub, is clear on where he stands: “If you accept false positives, it leads to customers losing trust in your product and causes unnecessary work for your call centres.”

If your false positive rate feels too high, the next step isn’t to jump to solutions. It’s about understanding what’s driving it and how you can stop it before you lose something sacred, like your customer’s trust in your institution.

1. Legacy rule-based systems struggle to keep up with modern transaction behaviour

Most transaction monitoring systems still rely, at least in part, on static rules. These rules were built to be explainable and auditable, and both still matter. However, transaction behaviour has outpaced the rules designed to monitor it.

Lack of adaptability

Fixed thresholds, such as flagging transactions above a certain value, make it challenging to distinguish between legitimate and suspicious transactions.

An outgoing £5,000 payment could be:

- A deposit to a builder for upcoming house construction work

- A gift to a loved one

- A fraudulent transfer

Without context, they look the same. That lack of distinction leads to unnecessary false positive alerts.

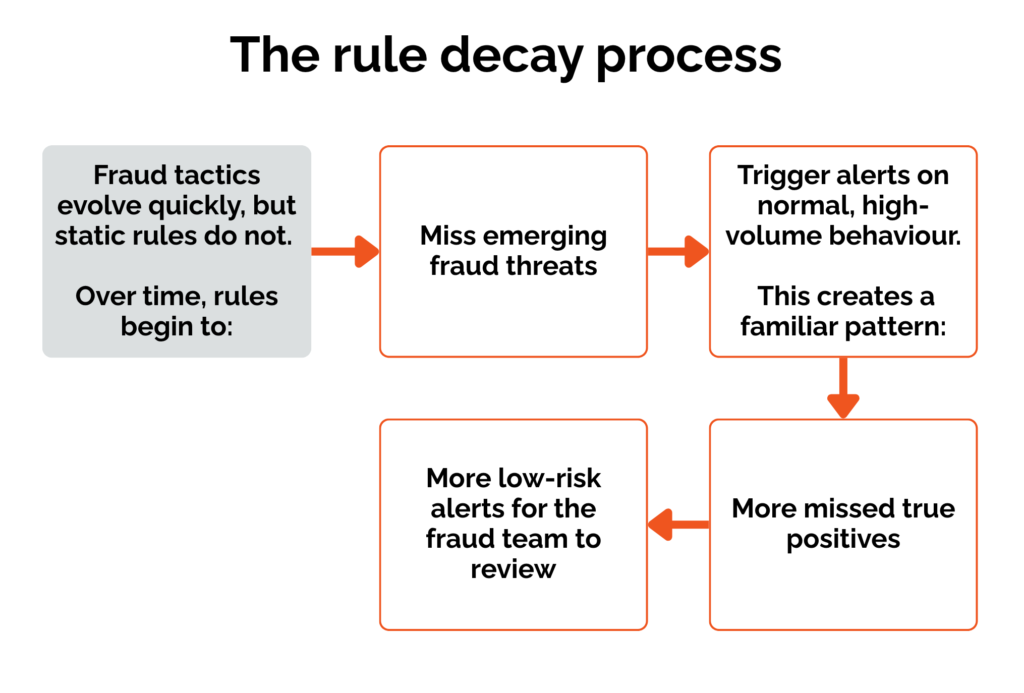

Rule decay

Fraud tactics evolve quickly, but static rules do not.

Over time, rules begin to miss emerging fraud threats and trigger alerts on normal, high-volume behaviour.

This creates a familiar pattern:

- More missed true positives

- More false positives and low-risk alerts for the fraud team to review

What to look for

- Alert volumes are increasing without a rise in fraud losses

- Repeated flags on known, trusted activity

- More time spent on manual review

These are signs that your rules are no longer aligned with real behaviour.

Where is this heading?

The institutions we work with are moving towards machine-learning fraud detection, where platforms adapt over time rather than relying solely on static thresholds.

Rules still play a role, but they cannot carry the full load anymore.

2. Over-tuning detection systems creates more noise than signal

No team wants to miss a genuine case of payment fraud. The consequences are clear: regulatory scrutiny, financial loss, and reputational damage.

The Financial Conduct Authority has issued significant fines to firms that failed to detect or prevent financial crime.

Since 2021, the regulator has issued fines totalling over £300 million to banks for failures in financial crime controls, reinforcing the seriousness with which missed fraud and weak monitoring are treated.

So institutions’ infrastructure is often tuned to be highly sensitive.

A familiar pattern

- A customer makes an unusual but legitimate purchase

- The system flags it as suspicious activity

- The transaction is blocked or delayed

- The customer contacts support

- The analyst clears it

At scale, this clunky workflow incurs high operational costs without reducing the risk of fraud. It also contributes to sustained alert fatigue, a growing issue happening across fintech institutions. Essentially, the more false alerts that an analyst deals with, the less important they seem, dragging down even the true fraud identified during the process.

The safety net trade-off

In practice, this means:

- Growing alert fatigue across compliance teams

- A higher false positive rate

- More alerts per transaction

The intention is clear: reduce risk. But the outcome is less helpful and reduces focus.

Matt offers a straightforward view: “You can avoid regulatory fines by simply tuning the model rather than over-tuning it. The clue’s in the name.”

What to look for

High alert volumes with low conversion to fraudulent transactions. This is where tunability within categorisation and enrichment changes the conversation.

Instead of setting a fixed level of sensitivity, teams can:

- Adjust coverage based on confidence

- Prioritise higher quality signals

- Respond to changing fraud risk

As Matt explains:

“Our tunable coverage allows us to tone down the coverage and filter out lower confidence predictions in favour of higher confidence predictions.”

3. A lack of contextual data leads to high-risk decisions

Even well-tuned models struggle without the right data.

In many cases, the root cause of false positives in fraud detection is not the model itself but the poorly-enriched data feeding it.

Many platforms still assess transactions in isolation, without considering real-time customer behaviour, historic income and spending patterns, or which other accounts, loans and financial products a customer might have access to.

Missing customer context

A transaction only makes sense when you understand the customer behind it. While a £25,000 transfer may be routine for a business owner, the same transaction may be unusual for a student.

Without insights into the specific customer profile, both appear risky. At the same time, banks can’t exactly afford to zoom into every single customer and transaction on a daily basis.

Matt shares a simple example of a recent fraud event that happened to him. He suddenly noticed banking app transactions from a record shop in Lithuania, despite never having visited the country or shopped online for records:

“If the bank is only looking at my credit card transactions in isolation, it might appear reasonable. But if that data is connected to my current account data, where you can see spending happening in another country, they can see that I can’t be in both places at once.”

“It’s the context that gets stripped away when the data is siloed.”

| What to watch out for? | What better looks like? |

| Repeated flags on consistent customer behaviour | Fewer legitimate payments are flagged |

| Inconsistent decisions across teams | Risk decisions become more precise |

| Heavy reliance on manual investigation | Fraud teams focus on genuine anomalies |

Moneyhub provides 98% accurate categorisation and enrichment data in real time, feeding directly into existing systems. This improves the quality of the signals your models rely on, without requiring a full rebuild.

You don’t have to drown in false positives

High false positive rates are not inevitable. With proper structure in place, they can help reduce alert fatigue for your fraud team.

Three factors usually drive them:

- Static rules applied to dynamic behaviour

- Overly sensitive tuning

- Incomplete or siloed data

Each one is solvable. The first step is identifying which of these is affecting your current transaction monitoring system. From there, the path forward becomes clearer.

But only once you know where the problem lies can you take the next step: reducing false positives to confidently identify fraud in real-time.

About Matt Barr

Matt Barr is a Product Director here at Moneyhub. He’s been working either with or for banks since the mid-00s, solving all manner of problems. From ISA transfers to corporate actions, Matt now focuses on transaction categorisation and enrichment. When he’s not solving client problems, you can find Matt buried under his children’s laundry or stomping through the Peak District.

share