Consumer Duty is a financial regulation in the UK that mandates financial institutions to meet ‘good outcomes’ across their customer groups. It aims to move the industry from tick-box compliance to a prudential regime that truly places the customer’s best interests at the heart of the business.

The FCA brought in Consumer Duty to prevent foreseeable harm for consumers, but some banks still need to upgrade their tech stack and data insights to deliver this higher standard of customer care. That’s where Moneyhub can help: providing a platform to collect and analyse a consumer’s personal financial data on an individual level, to help compliant financial institutions offer services that meet customer needs.

Key takeaways for Consumer Duty:

- FCA Consumer Duty is a UK-based regulation requiring financial institutions to create good customer outcomes

- Consumer Duty requires firms to check their products are suitable and of fair value, while they must communicate the benefits and risks clearly and offer reasonable support when customers are struggling financially

- Firms can comply with Consumer Duty through providing evidence of good vs poor outcomes, and gaining a holistic view of their customer’s full financial picture

Consumer Duty: what, when and why?

What is the regulation?

Consumer Duty is a regulation introduced by the Financial Conduct Authority. It covers one key principle: to deliver good outcomes across all customer groups, alongside three cross-cutting rules:

- Act in good faith

- Prevent foreseeable harm

- Support financial objectives

The Consumer Duty is an expectation on compliant firms to continuously monitor and evidence that they are delivering these ‘good outcomes’.

When was it introduced?

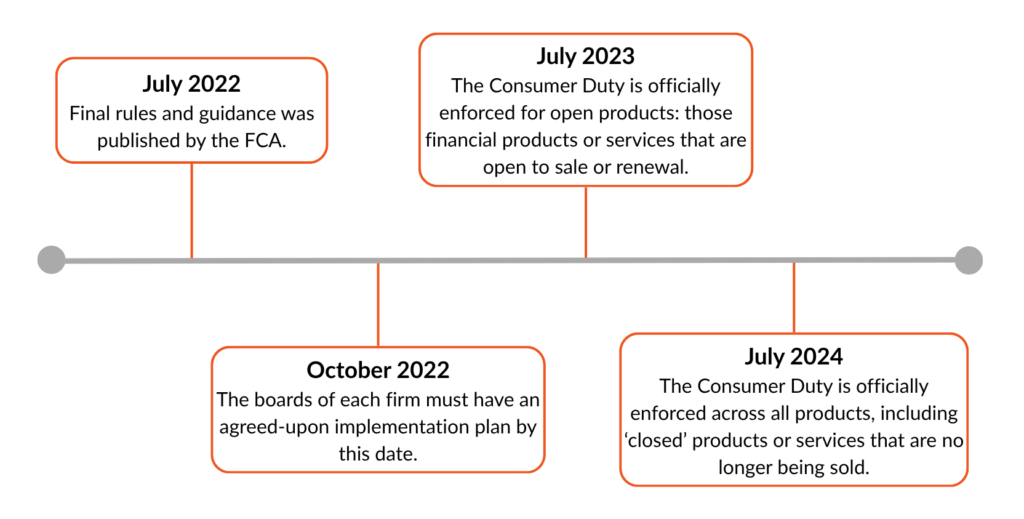

Here’s the timeline of Consumer Duty:

July 2022: Final rules and guidance was published by the FCA. Firms knew that the regulation was definitely coming, and could start preparing for its implementation deadline.

October 2022: The boards of each firm must have an agreed-upon implementation plan by this date.

July 2023: The Consumer Duty is officially enforced for open products: those financial products or services that are open to sale or renewal. Firms offering these products must have reviewed their alignment with Consumer Duty by this date.

July 2024: The Consumer Duty is officially enforced across all products, including ‘closed’ products or services that are no longer being sold.

Why was Consumer Duty introduced?

It was designed to restrict high-friction and predatory scenarios in the financial industry, providing a minimum standard for the customer experience.

In the UK, and despite a lot of progress after the 2008 recession, there is still a level of scepticism around financial products and services. For example, some consumers have felt duped by buy now, pay later schemes (BNPL) – not realising that a default on payments could affect their credit history, and future eligibility to borrow. Mis-selling scandals in the car finance space, mismatched investments compared to risk profiles, and complex account closure processes: each of these common scenarios have all contributed to the launch of Consumer Duty.

With a new outcomes-based approach, the Consumer Duty puts the onus on firms to evidence their good practices, and detail the occasions where they have stepped in to prevent harm. It shifts the customer experience, from relying on culture to enforcing tight controls. With a particular focus on vulnerable customers, which we will get into in the next section, ‘fair value’ must now extend across all groups, not just those able to clearly advocate for themselves.

(The FCA confirmed final rules on BNPL on February 11th 2026, and relies on Consumer Duty when it comes to this new regulation. Providers will need to do everything in line with its requirements.)

What are the key requirements of Consumer Duty?

Firms are expected to monitor and evidence their ‘good outcomes’ across four key consumer categories:

- Products and services: are products fit for purpose? Consider the needs, and financial objectives of the target market, and whether the product could cause foreseeable harm among some groups (suitability).

- Price and value: is the benefit received relative to the price paid? Products must offer demonstrable fair value.

- Consumer understanding: how clear is your communication? Consumers must be able to make informed financial decisions based on clear, timely and comprehensible product descriptions and instructions.

- Consumer support: how easy is it to get help, switch or cancel? Firms must consider the entire lifecycle, including life event triggers that change product suitability. And make it as easy and (cost-effective) to cancel as it was to sign up.

Examples of Consumer Duty rules in action

| Financial product | Pre-Consumer Duty practice | Rule | Post-Consumer Duty standard |

| Mortgages | Lenders could keep customers on high Standard Variable Rates indefinitely without proactive contact. | Price and value: firms must ensure a reasonable relationship between price and benefits. | Lenders must proactively alert customers when their deal ends and offer accessible paths to better-value products. |

| Financial products | Complex fine print or hidden fees that made it difficult for borrowers to understand the total cost of credit.The weight was on the buyer to take the burden of understanding, even if there were 40-page T&Cs documents which technically met disclosures but practically ensured consumers wouldn’t read them. | Consumer understanding: communications must be clear and enable customers to make informed decisions. | Agreements must use simplified language, highlighting total costs and risks prominently so the average borrower truly gets it. |

| Loans | Lenders often used Office for National Statistics (ONS) averages for living costs. If a consumer’s income was £2k and the ONS said the average person spent £1.2k, the lender assumed £800 was ‘affordable’, even if that specific individual had high childcare costs or hidden debts not on their credit file. | Price and value: institutions must act in good faith to avoid foreseeable harm. | Institutions must only lend what the consumer can afford to repay. |

| Savings | Customers let large sums sit in non-interest-bearing current accounts. | Customer objectives: firms must support customers in reaching their specific financial goals. | Banks could launch savings apps to help customers automatically sweep their money into an interest-gaining account, like Paragon have done with the Spring app |

| Credit cards | Account managers were incentivised to sell based on volume rather than suitability, which risked a culture of mis-selling. | Governance and culture: firms must implement policies so that delivering good customer outcomes is rewarded more than sales volume. | Bonuses are now balanced with quality/suitability metrics, such as low delinquency rates or customer satisfaction scores. |

| Insurance | Price walking was common practice, automatically increasing premiums for loyal customers at renewal while offering cheap deals to new joiners. | Cross-cutting rules: firms must act in good faith and avoid causing foreseeable harm. | Renewal prices must be transparently compared to new-customer prices, ensuring loyal customers aren’t penalised for staying. |

Who must comply with Consumer Duty?

The short answer: Consumer Duty applies to every firm regulated by the FCA. This includes banks and building societies, lenders and credit firms, insurance and pension providers, and payment services operators.

Due to the wide-spreading nature of Consumer Duty, though, the regulation applies up the distribution chain, too. And here comes the scary part: it applies even if the partner company never interacts directly with the end customer.

This is thanks to material influence: the idea that if a middle-man can affect the price, product design or product management, they must fall under the Consumer Duty requirements.

A scenario I’ve seen has been when a non-bank brand (like budgeting apps and even retail brands) offers current accounts or debit cards. The app or retail brand is the distributor, so they’re often an unregulated entity, partnering directly with the manufacturer: the bank or banking-as-a-service provider.

Imagine that the app heavily markets its current account to a young, low-income user with the promise of “instant access to your cash”.

Yet, the bank’s underlying legacy tech can’t support this, with:

- Frequent down times

- Overly aggressive automated fraud algorithms that freeze accounts without human customer service available

In this case, the manufacturer (the core bank) is causing foreseeable harm and failing on Consumer Support. Or if the distributor (the app) doesn’t adhere to the target market under Products and Services and uses misleading tactics to obscure certain fees, it is failing on Consumer Understanding.

“Under the Duty, the bank is obligated to audit the app’s marketing and the app is obligated to ensure it is aligned with the bank. Importantly, if one fails, the FCA holds the regulated entity accountable for the whole chain.” – Nejc Korosec, Head of Compliance at Moneyhub

How to comply with Consumer Duty?

For large firms, full compliance is expected through a range of reporting, auditing and governance strategies.

Annual board reports

Assessing whether they are indeed providing good outcomes, or where improvements must be made. Including factors like the number of customer complaints, cancellation rates and the analysis of different customer groups. Firms must also provide evidence of actions taken to address poor outcomes (or risks to poor outcomes).

Audits (internal)

Audits help firms to validate whether they are truly providing the ‘fair value’ that they might claim to be. Firms should assess:

- Process design, such as vulnerability support per cohort: how is the account opening process adapted for blind individuals, for example?

- Actual outcomes (to check whether the process design is correct) including fair value assessments and communications testing

- Risks and transparency in oversight: is there feedback data that you can’t access, or potential risks that you have not yet accounted for?

Senior Manager accountability

Consumer Duty is deeply connected to the Senior Managers and Certification Regime (SMCR), and as such, senior managers are personally accountable for ensuring their firms deliver on good outcomes.

Previously, the rules also stated that a Consumer Duty champion had to be appointed. This individual was responsible for advocating for consumer interests at a board level, holding the board accountable by acting as a bridge.

But this has recently changed:

“Since February 2025 this is no longer a requirement. The FCA found that having a single ‘champion’ allowed the rest of the board to pass the buck. Now, they expect the entire board to be collectively accountable.” – Nejc Korosec, Head of Compliance at Moneyhub

Renumeration policies

In my opinion, one of the strongest parts of the regulation is that firms can no longer incentivise or reward based on sales only. That’s because it may encourage and reward unsuitable products or cause foreseeable harm.

Now remuneration policies must be aligned to good customer outcomes, preventing mis-selling based on individual rewards.

Setting up your own systems and policies

At a smaller firm level, the FCA has acknowledged that the same resources may not be available. So while the requirements still apply, the regulator expects proportionality.

“Firms may have expected to use customer feedback and complaints as their primary monitoring tool, but the FCA has repeatedly stressed that complaints are reactive. And the Duty requires proactive monitoring to prevent foreseeable harm, even from smaller firms.” – Nejc Korosec, Head of Compliance at Moneyhub.

While the FCA allows for proportionality, even small firms must use proactive data instead of waiting for a customer to complain. For example, tracking how long a user spends on a terms and conditions page or monitoring cancellation rates are two of the strategies I see often.

The Consumer Duty is not a prescriptive regulation, due to its outcomes-based design. But this means the biggest risk for firms is information blindness: if you don’t have a clear view of your customer, how can you prove you’re helping them?

Moneyhub supports firms in their Consumer Duty compliance by moving firms from vague assumptions to verified data. We offer the ability to aggregate a customer’s entire financial life into a single view, with decisioning based on the data itself, not lagging ONS assumptions or segments that are too broad to use. And we give firms the ability to proactively intervene before the customer reaches a crisis point, fulfilling the Duty’s requirement to support vulnerable consumers.

Learn more about Data Aggregation.

What are the consequences of non-compliance?

Under the FCA’s watchful eye, violations of Consumer Duty are already resulting in fines of millions.

In one 2024 case, the Senior Manager of a pensions firm gave unsuitable pension transfer recommendations to over 900 customers, without assessing their risk profiles or attitudes to investment. He was fined over £1 million in violation of SMCR and Consumer Duty, effectively “choosing to prioritise the Firm’s profitability (which took over £8 million in fees) over the interests of its customers”.

But alongside the obvious financial implications, it’s the reputational impact of non-compliance that could do the most damage. In a similar case to the above where 15 individuals were banned from providing financial advice, the company at the heart of the scandal actually collapsed. The government was forced to take over and it was later sold on.

While these reputational consequences are typically more ‘hidden’ compared to the outright penalties, they are the most likely to erode trust with your customers, and cause you to lose market share to competitors.

Following Consumer Duty best practices as a strategy for customer engagement

Consumer Duty is the financial regulation that is changing the way that institutions interact with their customers: striving for good outcomes across all groups. But many firms lack the technology to effectively know what’s best for their customers, and nudge them into taking the right action, which is where Moneyhub can help.

FAQs

The Consumer Duty is built on four key outcomes that firms must deliver: Products and Services, Price and Value, Consumer Understanding, and Consumer Support. These outcomes ensure that financial products are fit for purpose, offer fair value for the cost, provide clear information for informed decisions, and offer accessible support throughout the customer journey.

Moneyhub aids financial institutions with their Consumer Duty compliance by providing the data insights and technical stack required to fully understand customers. We enable you to granularly zoom into customers on a personal level in order to segment accurately, send timely nudges and make the right product offers.

Non-compliant financial institutions face regulatory intervention from the FCA, including substantial fines, the withdrawal of permissions to operate, and mandatory requirements to pay redress to affected customers. Beyond these legal penalties, firms risk severe reputational damage and a loss of market trust that can undermine their long-term commercial viability.

About the author:

Nejc Korosec is Head of Compliance at Moneyhub, leading the company’s compliance function and overseeing regulatory strategy, governance and day-to-day regulatory matters. Hailing from Slovenia, where he was the Head of Compliance for two regional banks, Nejc has worked in AML fraud, investigations and regulations for over 12 years. Now, he is responsible for managing Moneyhub’s relationships with regulators and trade bodies, and for shaping the firm’s public policy engagement across key issues impacting open finance, data-sharing and better consumer outcomes.

share